Written by Maggie Tiede

Maggie Tiede is a writer and blogger based in Saint Paul, Minnesota. Maggie has worked as a freelance writer since 2013, when she began reporting on politics, local events, health, and human interest for the Grand Rapids Herald-Review.

Reviewed by Paul Martin

Paul Martin is the Director of Education and Development for Myron Steves, one of the largest, most respected insurance wholesalers in the southern U.S.

Updated октября 15, 2019

Save on Long Term Care Insurance

Our independent agents shop around to find you the best coverage.

Have you ever worried about what would happen if you needed to enter a nursing home or assisted living facility? How would you afford it? If so, you’re not alone. As Americans age, long-term care is more necessary than ever. Long-term care insurance ensures you’ll be able to pay for it.

This step-by-step guide cuts through the long-term care insurance jargon so you can shop confidently. Once you’re ready to buy, independent insurance agents are here to make the process even easier. They’re experts who specialize in helping you find the right coverage at the right price.

Long-term care insurance pays for long-term care (three months or more) if you ever need it. The most common long-term care includes stays in nursing homes, but some policies may also cover the costs of a home health aide, assisted living, or other professional long-term care arrangement.

Each insurance company does long-term care insurance a little differently. There’s a lot of variation in what these policies cost, what they cover, and when they can be used. An independent insurance agent can help you shop around between companies.

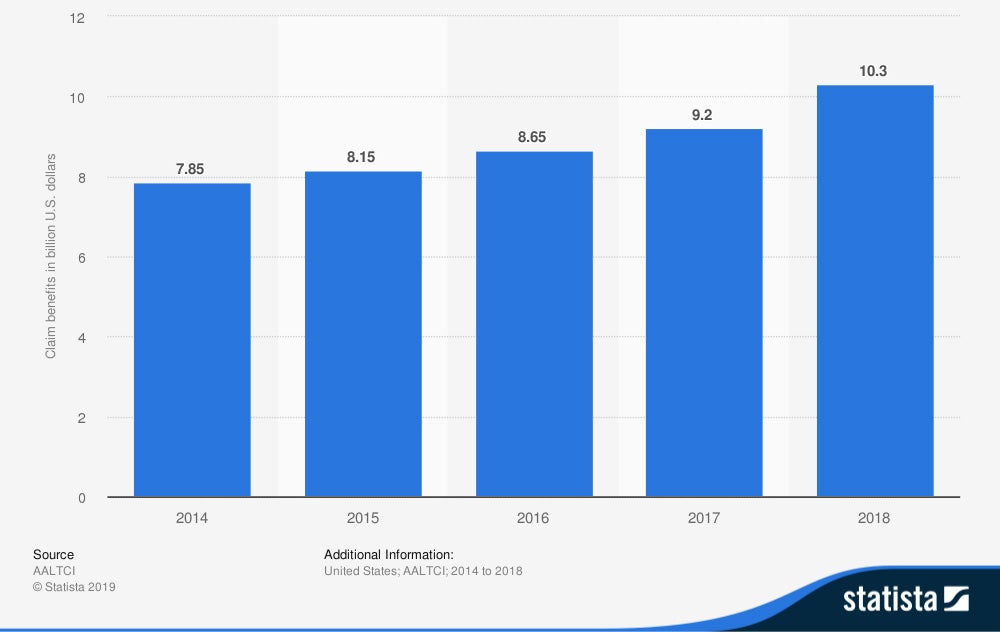

Long-term care insurance companies paid out over 10 billion in benefits to their customers in 2018 alone. The cost of long-term care is rising, making long-term care insurance an important way to secure your retirement.

Long-term care means help with day-to-day tasks and medical care received over the course of three months or more. This includes tasks like:

Long-term care can come from friends and family or from professional sources like nursing homes, assisted living facilities, and home health aides. Long-term care insurance covers the cost of professional care.

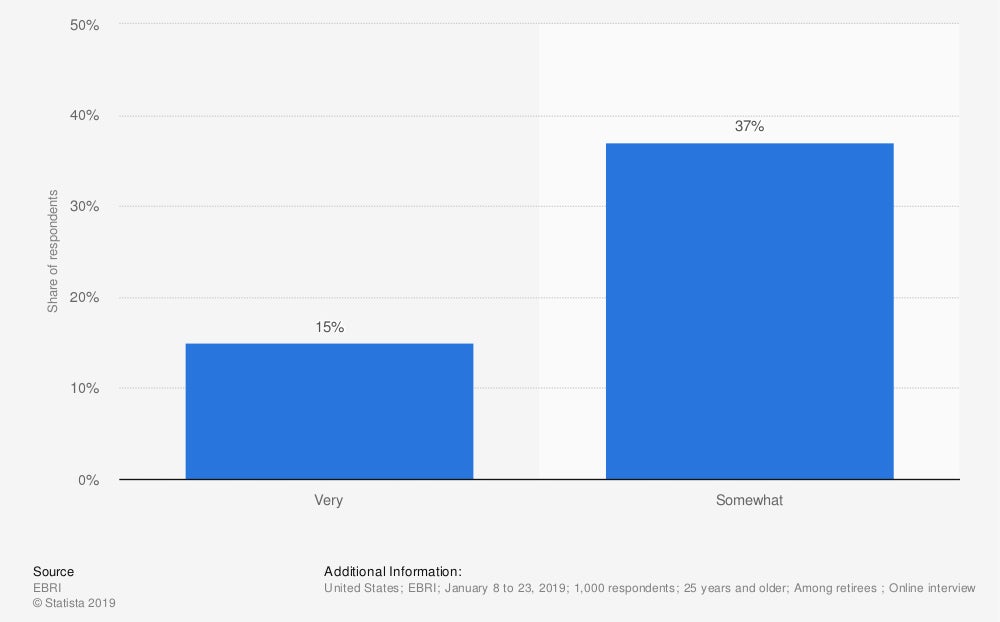

As of 2019, only 15% of retirees were “very” confident they could afford long-term care, with 37% being “somewhat” confident. That means nearly half of retirees aren’t confident about whether or not they would be able to pay for long-term care if they needed it.

Even the people who are confident they’ll be able to afford it might not be planning for the correct cost. A recent study found that more than half of Americans over 40 underestimated the average cost of one month of nursing home care ($7,000 in 2017).

For all these reasons, long-term care insurance is the best way to ensure that you’ll be able to afford long-term care if you ever need it.

Save on Long Term Care Insurance

Our independent agents shop around to find you the best coverage.

Everyone can benefit from at least considering long-term care insurance since it’s estimated that nearly 70% of today’s 65-year-olds will need long-term care.

Long-term care insurance typically costs between $1,000-$10,000 per year in premiums. Three major things affect that cost: how old you are, the amount of coverage you would like, and where you live.

For people in their 70s or older, the cost of long-term care insurance can soar well above $10,000. The earlier you can purchase long-term care insurance the better.

The perfect window to buy long-term care insurance is between 40 to 65 years old. That’s when you’re old enough to be firming up retirement plans but young enough to still get affordable coverage.

Some companies offer discounts if you buy long-term care insurance as a couple instead of individually. If you and your spouse both want long-term care insurance, try shopping jointly to save money.

There are two main types of long-term care insurance: traditional and hybrid. Which one you choose affects both your premiums and your benefits.

Hybrid long-term care insurance is popular because it tends to be more cost-effective and flexible than traditional long-term care insurance. Hybrid policies guarantee you a benefit whether or not you ever need long-term care, so you’re hedging your bets by buying it.

Hybrid policies can also make more efficient use of your premiums than traditional policies can, which means you get more benefit for less money. Here’s how hybrid policies typically work:

Hybrid policies have lots of perks, but traditional long-term care insurance can still be a better choice for some people. An independent insurance agent can go over your insurance needs with you to help you decide.

Save on Long Term Care Insurance

Our independent agents shop around to find you the best coverage.

Now you know what long-term care insurance is and why you should buy it. Here’s how to actually get a policy:

The government website LongTermCare.gov keeps up-to-date statistics on the average cost of long-term care. You can also do your own research on local long-term care options you’re interested in.

Then think about how much of that daily cost you’d be able to cover yourself (from savings or other sources) and for how long. If there’s a shortfall, that’s how much long-term care insurance you should buy.

Armed with the numbers, set up a meeting by phone or in person to discuss long-term care insurance. This is also a great time to discuss life insurance and disability insurance. All three are closely related and you may receive a discount by bundling them together.

Look for an independent insurance agent who has experience in life insurance. Many life insurance agents also offer financial planning. Be sure to take them up on it if they do! Solid financial planning will help you get the most bang for your buck with long-term care insurance.

This is where an independent insurance agent really shines. If you already know which one you want, they can start getting quotes right away. But if you’re not sure, they can shop around multiple offerings with you and go over the pros and cons of each.

Remember that different companies have drastically different long-term care insurance options. Having someone on your side rather than on one company’s side is a big plus when it comes to choosing either traditional or hybrid coverage.

Insurance companies need your demographic and health information before they can give you a quote. (That’s because your unique health risks determine what they’ll charge you.) You can do this on paper or in an online questionnaire. This process may include a medical exam.

Sometimes you can do the exam in the comfort of your home. A doctor or nurse may be able to come to you. Be sure to ask your agent whether or not a home visit is an option.

Once you’ve finished up the red tape, your independent insurance agent can assemble quotes. Now’s the time to read the fine print on each one with your agent’s help, if you want it. Be sure to look out for:

Ask lots of questions of both your agent and the insurance companies. Think of long-term care insurance as a financial investment — because it is one — and take plenty of time to make sure you’re making a good one.

Cheap premiums don’t always mean a good deal. Look at the quote holistically to make sure you’re getting as much benefit out of your premiums as possible.

Once you’ve made a decision, sign the contract and breathe easy. You’ve just taken an important step toward securing your financial future.

Save on Long Term Care Insurance

Our independent agents shop around to find you the best coverage.

Independent insurance agents are unique. While captive insurance agents can only sell insurance from one company, independent insurance agents can shop around between multiple companies to find the real right deal for you, not just one company’s “best” deal.

With an independent insurance agent, you can be sure you’re talking to a real expert who knows long-term care insurance inside and out. Good luck shopping for this critical coverage.